Health Net uses cookies. By continuing to use our site, you agree to our Privacy Policy and Terms of Use.

Skip to Main Content

- Our Health Plans show Our Health Plans menu

-

For Members

show For Members menu

-

- Member Login

- Members Overview

- Pay My Bill

- Frequently Asked Questions

- Forms and Brochures

- My Health Pays Program

- Member Perks

- Behavioral Health

- Health Support Programs

- Your Wellness

- Flu Vaccine

- Access to Care

- Maternity & Family Planning

- Stay Covered

- Appeals and Grievances

- Tax Information

- Confidential Communication Request

- Interoperability and Patient Access

- Learn More

-

- Pharmacy show Pharmacy menu

Health Net uses cookies. By continuing to use our site, you agree to our Privacy Policy and Terms of Use.

Main Menu

- Our Health Plans show Our Health Plans menu

-

For Members

show For Members menu

-

- Member Login

- Members Overview

- Pay My Bill

- Frequently Asked Questions

- Forms and Brochures

- My Health Pays Program

- Member Perks

- Behavioral Health

- Health Support Programs

- Your Wellness

- Flu Vaccine

- Access to Care

- Maternity & Family Planning

- Stay Covered

- Appeals and Grievances

- Tax Information

- Confidential Communication Request

- Interoperability and Patient Access

- Learn More

-

- Pharmacy show Pharmacy menu

Know Your Costs and Coverage Levels

Health coverage costs include paying for your plan and paying for some of your care. Here's how it works.

- Monthly Premium

This is what you pay to keep your health coverage current. You pay it directly to Health Net. You pay it monthly, whether you use services or not. - Copayment or coinsurance

This is the amount you pay when you use health services. You pay it directly to the doctor, pharmacy or other provider (e.g., lab, hospital).

Some health plans have a deductible. A deductible is the amount you owe for some covered healthcare services before your health plan begins to pay for certain services.

The right level of coverage for you depends on your healthcare needs. It also depends on your budget and how you like to plan.

Know Your Healthcare Costs (Health Net 101) (duration 3:58)

Understanding what you pay and when.

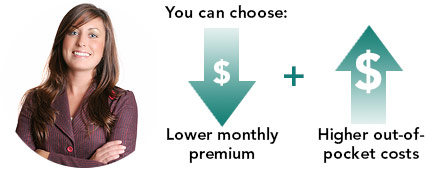

There is a tradeoff between the price of your monthly premium and the amount you pay when you need medical care.

Lee is 27 and rarely ill. She wants a health plan that keeps her covered but costs her less each month.

She picks a lower premium plan. She plans to put money aside in case she has an unexpected health expense.

Sam is in his early 50s and sees the doctor often for high blood pressure. He has had a couple of surgeries and may need another.

Sam chooses a plan with a higher monthly premium to keep his costs lower for the services he uses.